![]()

This article is for:

- ABSS Premier v21 and above

- ABSS Accounting v26 and above

Customer accounting for certain prescribed goods will be implemented from 1st January 2019 to deter fraud schemes where the seller absconds with the GST collected, but businesses further down the supply chain continue to claim the input tax. The prescribed goods are mobile phones, memory cards and off-the-shelf software, which are commonly used in these fraud schemes.

From 1 January 2019, customer accounting is required to be applied on a relevant supply of prescribed goods made to a GST-registered customer for his business purpose. A relevant supply is:

- a local sale of prescribed goods whose GST-exclusive sale value exceeds $10,000 in a single invoice

- and is not an excepted supply.

Under customer accounting, the responsibility to account for output tax on the supply shifts from the supplier to the customer.

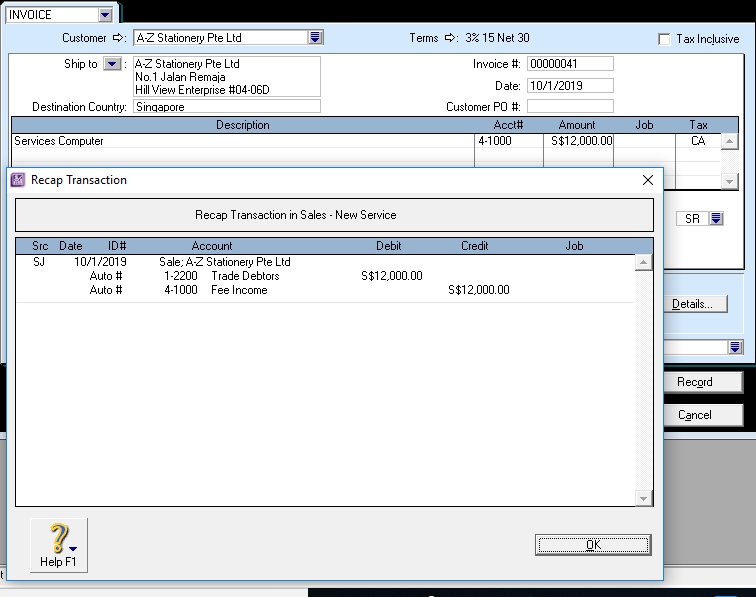

Recording sales using Customer Accounting

To record the sales transaction you need to record with the CA tax code. ( as the image below)

Even though the customer account tax code is 7%, however, there is no double entry for tax occur once you record this transaction. This because you not collected any output tax from the customer.

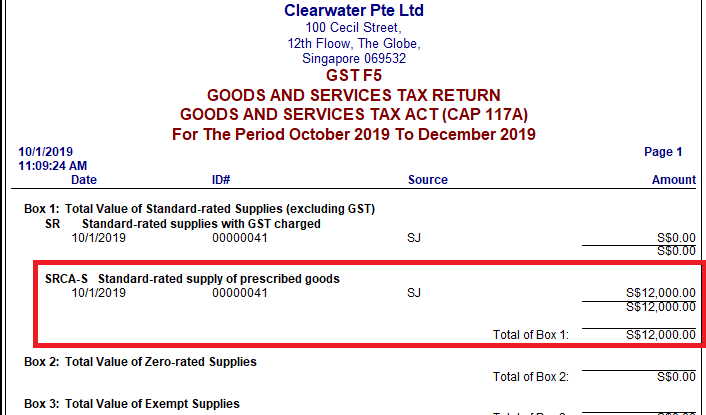

Once you record a sales using CA tax code, it will appear in GST F5 Box 1.

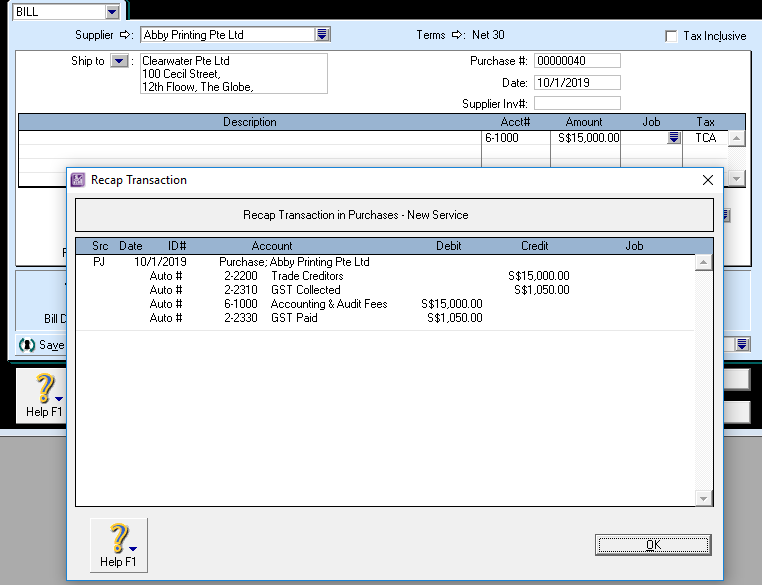

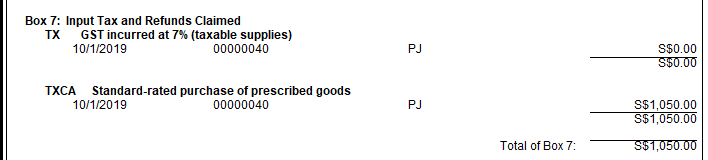

Recording Purchases using Customer Accounting

To record the purchases transaction you need to record with the TX-CA tax code. ( as the image below)

When you are using the tax code TX-CA ( TCA), the system will do the reversal of double entry. As per the example above, once you record the purchase amount $15,000 so the tax amount for GST is $1,050, which is 7% from $15000. This 7% will go to GST paid amount. Since this is the reverse charge mechanism, so the system will pass another journal to GST Collected with the same GST amount.

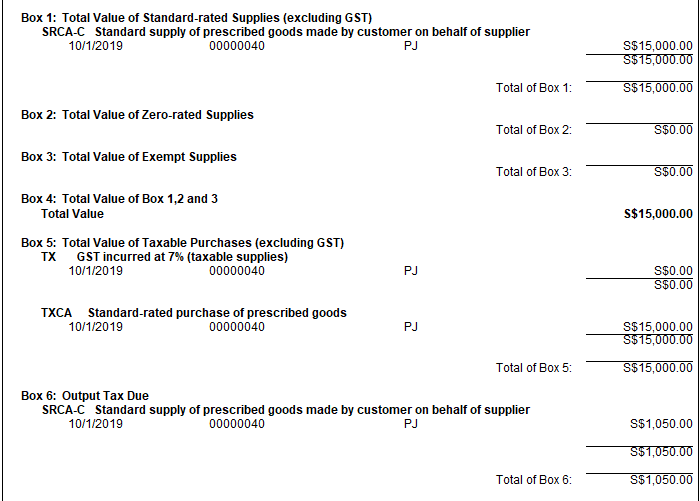

This tax code will appear in box 1,5,6 and 7 inside GST F5.

Comments

0 comments

Please sign in to leave a comment.